- The two Emirates currently have 626,887 sq m of retail space under construction

- Global shopping centre development increases to 41.9 million square metres

Dubai, 9 May 2016 – Two of the UAE’s most popular destinations, Abu Dhabi and Dubai, have together ranked amongst the top 17 of the most active cities for shopping centre development, according to CBRE’s latest Global Shopping Centre Development report. The cities currently have a total of 626,887 sq m of total retail space under construction, an 11% rise on last year’s figures. Dubai accounts for 361,127 sq m and Abu Dhabi for 265,760 sq m of retail space.

Dubai, 9 May 2016 – Two of the UAE’s most popular destinations, Abu Dhabi and Dubai, have together ranked amongst the top 17 of the most active cities for shopping centre development, according to CBRE’s latest Global Shopping Centre Development report. The cities currently have a total of 626,887 sq m of total retail space under construction, an 11% rise on last year’s figures. Dubai accounts for 361,127 sq m and Abu Dhabi for 265,760 sq m of retail space.

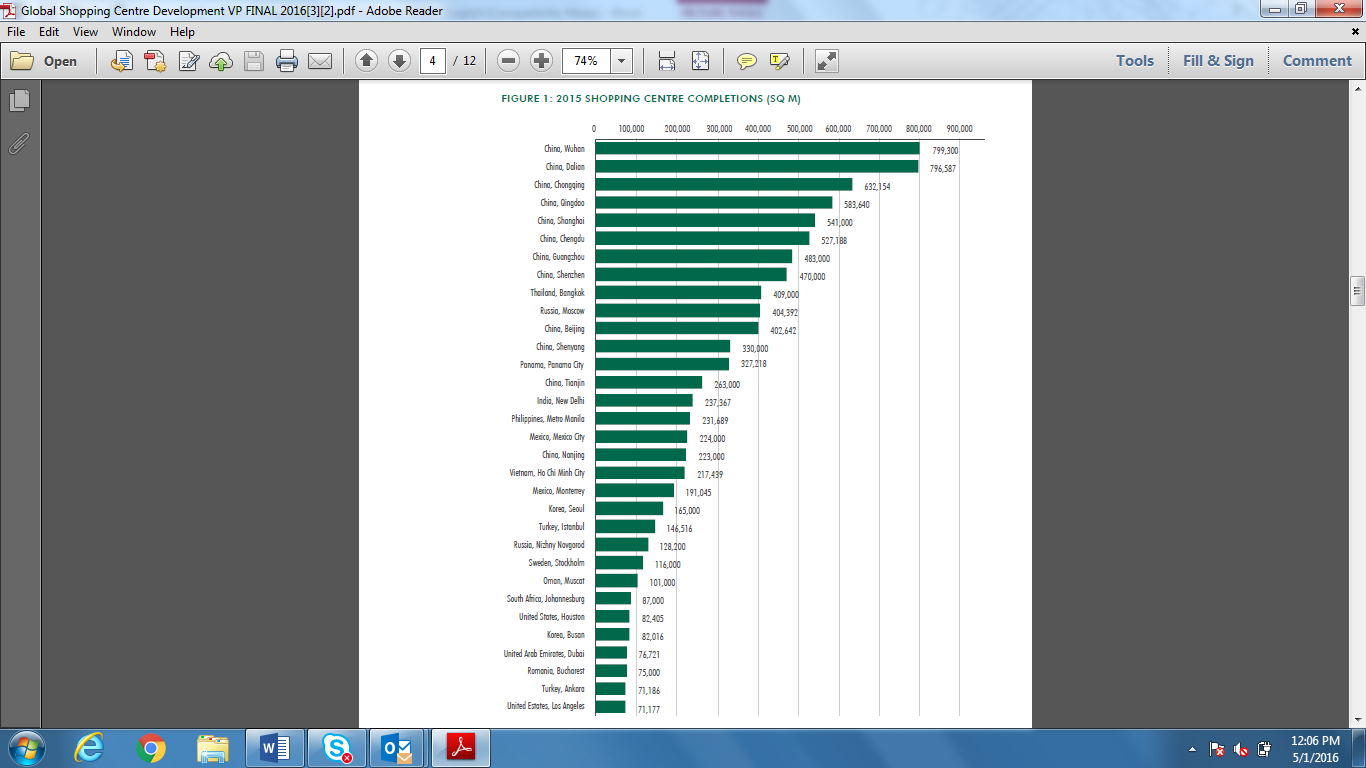

In the global rankings for shopping centres delivered over the last year, Dubai, along with Muscat, ranked in the top 30, with Muscat leading the way for the GCC region ( please see figure 1 below)

According to the 2016 report, the Middle East retail market remains a very attractive proposition for international brands. Dubai ranks second for international brand presence*, with high per capita incomes, significant growth potential, and a high spending consumer base.

Commenting on the findings, Matthew Green, Head of Research and Consulting, CBRE Middle East said, “We know that consumers across the Middle East like to spend their money on retail, food and beverage (F&B) and leisure activities particularly within the mall environment. The ongoing investment across the region is therefore catering to these needs and with retailers from across Europe and the U.S. continuing to look for alternatives to drive future expansion, the region offers a wide range of opportunities for consumers.”

“The Middle East offers a tried and tested marketplace for investors with less risk than those normally associated with emerging markets. This is clearly reflected in the size of the development pipeline for the region, especially so for Dubai and Abu Dhabi. With demand for new stores being sustained across key markets, developers remain bullish on the outlook for the retail sector in the region”, said Green.

Within the Middle East, the UAE’s development pipeline is significant with a number of major malls set out for delivery over the next three years. Nakheel’s Palm Mall in Dubai, which comprises around 111,000 sq m of GLA and is expected to complete in 2018, and The Point, which has a total GLA of 48,000 sq m and is due to open in 2017. In Abu Dhabi the next super-regional shopping mall expected to be completed is Maryah Central, which will offer around 146,000 sq m GLA.

The report also outlines that Doha is currently witnessing a transformation of its retail sector amidst an ongoing construction boom, which could see around 1.2 million sq m GLA delivered over the next three years alone, with the government striving to modernise the city in the build up to the 2022 Qatar World Cup. At nearly 264,000 sq m GLA, Doha Festival City, due to open in late 2016, is also set to become the largest mall in the country, featuring around 550 retail shops, including over 100 F&B Beverage outlets. The mixed-used scheme will combine retail with leisure, dining, entertainment and hospitality, including Doha’s first snow park as well as the region’s first Angry Birds indoor/outdoor theme park, and a theme park dedicated to the rapidly growing ‘gaming’ community.

Other results beyond the Middle East region unveil that China remains the most active market in terms of delivery of new space, accounting for two thirds of construction globally. Cities such as Chongquing, Shenzen, Chengdu and Shanghai all have over 3 million sq m of space under construction in over 30 projects in each city.

Emerging markets such as Manila, Moscow, Mexico City and Bangalore completed over 6 million sq m in 2015, however activity in Eastern European markets has slowed due to economic and political uncertainty.

The Global Shopping Centre pipeline continues to increase from 39 million sq m in 2014 to 41.9 million with Asian cities dominating nine out of the top ten most active global markets, reports leading global real estate advisor CBRE.