Modern Islamic finance is a young industry that has been attracting

Muslims looking to invest based on Islamic principles, and also appeals to

non-Muslims looking to diversify their portfolios by tapping into an attractive

pool of investment resources. Mohieddine Kronfol, chief investment officer,

Franklin Templeton Global Sukuk and MENA Fixed Income Strategies, provides an

overview of recent developments in Islamic finance and touches on some of the

challenges involving the standardisation—and regulation—of these instruments.

{kind=link}

Mohieddine (Dino) Kronfol

Chief Investment Officer

Franklin Templeton Global Sukuk

and MENA Fixed Income Strategies

Chief Investment Officer

Franklin Templeton Global Sukuk

and MENA Fixed Income Strategies

The Development of Shariah Compliance

Standards

The concepts underlying Islamic

finance are very old; indeed, many aspects of the Western

financial system that began to develop in renaissance Italy had Islamic roots.

However, modern Islamic finance is a relatively young industry with its first

stirrings in the 1960s and the first emergence of Islamic banks in the 1970s.

Having been established to meet religiously motivated requirements,

early Islamic institutions differentiated themselves largely by the purity of

their adherence to Shariah principles; specific jurisdictions tended to develop

their own interpretations of Shariah principles, although agreeing on the

fundamentals.

In recent years, the Shariah finance industry has expanded to include

many individuals looking to invest based on Islamic principles, but also

seeking a satisfactory return, and, to an increasing extent, non-Muslims

looking to tap into an attractive pool of investments. The development has led

to calls for increased regulation and standardisation of Islamic products, with

initiatives being undertaken by a number of authorities. In our opinion, the

drive towards regulation and standardisation should be treated with caution as

prescriptive standards could stifle innovation, while the Islamic community’s

emphasis on individual understanding and lack of a central authority means that

the goal of universally acceptable standards may be difficult to attain.

Rather, we would advocate the development of principal standards that would

leave room for innovation, while increased transparency amongst individual

practitioners would enable market participants to make clear judgments about

the acceptability of their products.

Global Reach of Islamic Finance

Although the roots of the Islamic finance industry are in banking

services—and bank deposits remain by far the largest source of

Shariah-compliant assets—other types of assets have become increasingly

significant, particularly for the Islamic asset management industry.

Shariah-compliant equity funds were an early diversification from the original

bank-based business. Takaful, an Islamic product akin to insurance, has

been growing in significance, while financial professionals have been

investigating ways to bring Waqf, or Islamic endowments (currently

largely based on property) into the financial mainstream. Perhaps the most

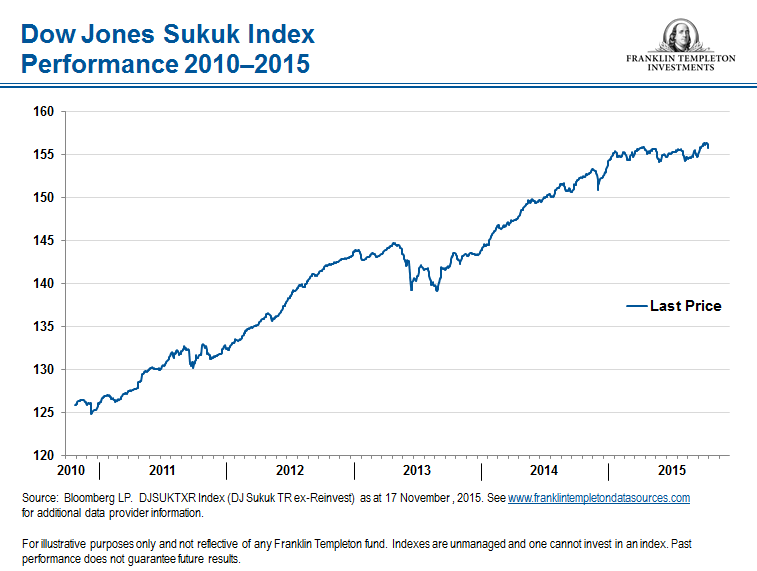

dynamic area of development is in Sukuk, commonly referred to as Islamic

bonds, an asset type that has been seeing rapid growth and that has tended to

be the principal area of activity as different financial centres look to

capture shares of what is seen as a fast-growing market.

What Are Sukuk?

Sukuk is the plural of the Arabic word Sak,

literally translated as title deed. They are financial certificates structured

to comply with Islam’s prohibition on the charging or paying of interest (known

as Riba) that grant an undivided interest or share in an underlying

asset along with the profits, cash flows and risk commensurate with such

ownership. Sukuk are often referred to as the Islamic equivalent of bonds.

While a conventional bond is a promise to repay a loan, Sukuk constitute

partial ownership in a lease (Sukuk Al Ijara), a business or a

partnership (Sukuk Al Musharaka), receivables (Sukuk Al Murabaha),

a project (Sukuk Al Istisna), or an investment (Sukuk Al Istithmar).

In other words, Sukuk represent ownership of real assets, whereas conventional

bondholders own debt.

The three most popular Sukuk contracts by issuance volume are Sukuk Al

Ijara, Sukuk Al Musharaka and Sukuk Al Murabaha.

- Sukuk Al Ijara are sale-and-leaseback structures that use revenues from an underlying asset such as a building to pay investors.

- Sukuk Al Musharaka are derived from the word “Shirkah,” meaning partnership, in which all partners contribute capital and labour. Profit is shared among partners at an agreed-upon ratio or a declining basis. Losses, however, are shared in proportion to the contributed capital.

- Sukuk Al Murabaha refer to a contractual agreement according to which a financier buys a good or an investment and then sells it to a customer with a markup on a deferred basis.

At present, Malaysia leads the industry with US$164 billion in issued

Sukuk in 2014, representing more than 60% of the overall market. London was a

distant second with US$38 billion1 and Dubai third with US$21.1 billion,2 with both cities striving to close

that gap. London has shown a willingness to accommodate Sukuk in the tax code,

and offers strength in ancillary services such as legal, insurance and

educational resources rooted in its significance as a historical centre of

conventional finance. Dubai is looking to build on its strengths as a major

trading and travel hub through a holistic approach to Islamic economic

activity, seeking to dominate industries such as Halal (permitted under

Shariah law) food and Islamic tourism as well as finance. At the same time,

Dubai’s government has been active in promoting the emirate as an Islamic

economic centre by influencing businesses with links to the state to raise

finance through Sukuk issuance. Indeed, in terms of listing Sukuk on domestic

exchanges, Dubai has passed Malaysia, according to Nasdaq Dubai.

Meanwhile, smaller players are also looking for a share of the market.

Dubai is being challenged in the Middle East by markets such as Qatar, Oman and

even its neighbor in the United Arab Emirates (UAE), Abu Dhabi. And, Bahrain

has long sought a role as an arbiter of Shariah adherence. The Accounting and

Auditing Organization for Islamic Financials Institutions (AAOIFI), established

in Bahrain in 1990, is probably the nearest the industry comes to an

internationally recognized authority. Turkey and Tunisia are also looking to

build Islamic finance industries. In Europe, Dublin and Luxembourg are looking

to take market share from London, while Johannesburg is aiming to establish

itself as the leading Sub-Saharan African centre for Islamic finance, in

competition with Lagos. In Asia, Indonesia is starting to compete with

Malaysia, while Hong Kong is emerging as a potentially important centre for

Sukuk issuance. In all, approximately 30 countries worldwide have issued one or

more Sukuk.

{kind=link}

Saudi Market and Islamic Finance

The emergence of two previously reclusive Islamic powerhouses—Saudi

Arabia and Iran–could have a significant impact on the development of Islamic

finance. As a leader of Islamic thought in the Middle East and globally, Saudi

Arabia’s interpretations of Islam as it relates to financial affairs could

become influential. Although its equity market’s opening to international

investors is quite restricted at present, and the Sukuk opening is still to

come, we believe that over time both will extend and become transformative not

just for Saudi Arabia but the Middle East as a whole. We would anticipate that

the experience of catering to international investors will likely lead to

improvements in regulation, transparency and product structuring that will

render both Shariah equity and domestic Sukuk markets in Saudi Arabia

increasingly appealing to Sukuk investors.

Iran, meanwhile, is the domicile of the largest stock of Islamic assets

globally, as a result of banning the payment of interest throughout its banking

system in 1983.3 After exclusion from global financial markets for

many years, partly through choice and partly due to sanctions, the recent

accord with the international community over nuclear industry development could

open the way for sanctions to lift and for Iran to participate in the global

Islamic finance industry. The reintegration of Iran into global Shariah markets

could be of immense significance, in our opinion.

Development and Innovation within Shariah Markets

The Islamic banking system is itself seeing some interesting new

developments that could extend the reach of more sophisticated

Shariah-compliant products. Evolving banking solvency requirements are driving

demand for subordinate, perpetual and lower-tier Sukuk as banks that previously

held reserves largely in cash deposits at central banks look for more efficient

balance sheet structures, which has the effect of widening investment choices

for outside investors.

On the liability side, the Malaysian government recently launched an

initiative relating to bank deposits, still the largest portion of

Shariah-compliant assets overall, that could expand the scope of Sukuk,

particularly if the Malaysian example is followed elsewhere. The Islamic

Financial Services Act of 2013 is a measure aimed at modernising and clarifying

earlier legislation on Islamic Finance. Measures involving deposits invoked an

explicit division between contracts with capital guarantees (deposit accounts)

and those without (investment accounts), with the latter no longer eligible for

protection under the government’s deposit insurance scheme.

The new regulations are due to be finalised shortly and represent an

interesting experiment to test whether depositors are prepared to accept a

measure of capital risk in exchange for more returns, or whether the

traditional role of banks as custodians of their clients’ money will dominate,

leaving the investment account structures to wither away and Islamic banks less

differentiated from their conventional counterparts.

Implications for International Investors

As the number of centres of Islamic finance grows, questions around

local interpretation could increase, though, in our opinion, the difficulties

sometimes appear overstated. Even leaving aside the special case of Iran, local

finance traditions in many Islamic countries differ in some respects.

Non-Islamic majority countries, such as the United Kingdom and Hong Kong,

present different issues. Although such countries naturally tend to avoid

controversial interpretations of Shariah as they bid to establish themselves,

the activities of sophisticated financial professionals can lead to the

development of innovative products that can require interpretation. The

challenge for Islamic finance is to achieve a degree of uniformity in the

treatment of assets, providing comfort to international investors, when the

underlying principles governing such treatments necessarily have local roots.

For many practitioners of Islamic finance, the solution to the issue of

variability of interpretation is the establishment of detailed common

standards. A number of countries with large Shariah-compliant financial

industries have moved to establish national Shariah boards to provide specific

standards for products within their jurisdiction. Malaysia led the way in 1997,

while in more recent years, countries including Indonesia, Oman, Pakistan,

Nigeria and Morocco have established or announced similar bodies. Recently, the

UAE joined the trend announcing its intention to have a federal Shariah board.4 The Dubai Financial Market followed a slightly

different route, announcing specific guidelines for Sukuk issuance in April

2014 that complemented a 2007 document dealing with issuing and trading shares

in a Shariah-compliant fashion.

Many commentators have called for global Shariah standards to be

established. The emergence of national and international Shariah boards has

been seen as a positive development. Although they can provide solid guidance

to originators and users of financial products, they come with their own

problems. A further issue with national and international boards is that

detailed discussions and a search for consensus can be time consuming. A

standard for currency hedging took some seven to 10 years to be established,

for example. With the Sukuk market developing quickly, a standard can become

outdated with new product features simply not envisaged at the time of

promulgation, creating an appearance of non-adherence. Faced with commercial

pressures to issue products, banks will often go their own way rather than

await guidance from the national board.

An Alternative Approach—Principal Standards and

Practitioner-Driven Solutions

We agree that the development of accepted international standards is an

important step required if Islamic finance is to fulfill its current promise

and become a truly global industry. To that end, well-resourced and

professionally supported Shariah boards have value in speeding up decision-making.

We would support the development of principal standards, clearly stating

unacceptable practices, but otherwise leaving room for interpretation and

development. The onus then falls on product originators to be as transparent as

possible in laying down the nature of their products and their rationale in

Islamic law. Potential buyers of the products can then clearly understand what

is being offered and why. As long as the legal theory underpinning particular

products is clearly mapped out in the prospectus, the product can then prosper

or fail according to its acceptability within the industry. Over time, a

market-driven consensus on the structure of Islamic products should become

clear.

At Franklin Templeton, we have adopted strategies to ensure Shariah

compliance that we believe represent industry best practice. Our Shariah board

is made up of distinguished scholars drawn from a variety of Islamic

traditions. The scholars provide initial approval on investment objectives and

strategy, as well as ongoing supervisory and monitoring services to ensure

continuous adherence to internationally accepted Shariah principles and

standards. Some 40,000 individual securities are monitored for Shariah

compliance using sophisticated algorithms to drill down into their business

activities and balance sheet structure. For those businesses with acceptable

primary functions, but some involvement in haram (prohibited) activities, we

are able to isolate the haram income streams and confirm necessary purification

payments. As it regards our Sukuk activities, the scholars are involved on a

security-by-security basis, and all derivative products that are considered are

also investigated and approved. To further improve our transparency, we are in

the process of creating a Sukuk rulebook that will clearly document our

standards. The rulebook will allow interested parties to understand clearly the

nature of the products that we deem acceptable and the rationale for our views.

The Shariah boards of potential customers will be able to make a fully informed

decision on whether to invest.

An Evolving Asset Class

The growth of Islamic finance in terms of both value and the

proliferation of countries participating clearly demonstrates to us solid and

sustainable levels of demand for the industry and its underlying values. The

widening geographic spread and technical complexity of the Islamic finance

industry have led to a desire for uniformity of interpretation that is hard to

achieve given the many different Islamic traditions that have to be taken into

account. Although we understand the calls to supply definitive standards

through the establishment of national and international Shariah boards, we

would caution against over-prescriptive regulation. In our opinion, with the

freedom to innovate and with sufficient transparency shown by product

originators, the community of Islamic finance participants can evolve by

consensus to produce satisfactory, market-based solutions so that the industry

can become both a strong competitor to conventional finance and a source of

unique investment options that can appeal both to Islamic and conventional

investors.

Mohieddine Kronfol’s comments, opinions and

analyses are for informational purposes only and should not be considered

individual investment advice or recommendations to invest in any security or to

adopt any investment strategy. Because market and economic conditions are

subject to rapid change, comments, opinions and analyses are rendered as of the

date of the posting and may change without notice. The material is not intended

as a complete analysis of every material fact regarding any country, region,

market, industry, investment or strategy.

Data from third-party sources may have been used in

the preparation of this material and Franklin Templeton Investments (“FTI”) has

not independently verified, validated or audited such data. FTI accepts no

liability whatsoever for any loss arising from use of this information, and

reliance upon the comments, opinions and analyses in the material is at the

sole discretion of the user. Products, services and information may not be

available in all jurisdictions and are offered by FTI affiliates and/or their

distributors as local laws and regulations permit. Please consult your own

professional adviser for further information on availability of products and

services in your jurisdiction.

To get insights from Franklin Templeton delivered to your inbox,

subscribe to the Beyond Bulls &

Bears blog.

What Are the Risks?

All investments involve risks, including possible

loss of principal. The value of investments can go down as well as up, and

investors may not get back the full amount invested. Bond prices generally move in the opposite direction of interest

rates. Thus, as the prices of bonds in an investment portfolio adjust to a rise

in interest rates, the value of the portfolio may decline. Special risks are

associated with foreign investing, including currency fluctuations, economic

instability and political developments. Investments in developing markets

involve heightened risks related to the same factors, in addition to those

associated with their relatively small size, lesser liquidity and lack of

established legal, political, business and social frameworks to support

securities markets. Such investments could experience significant price

volatility in any given year.